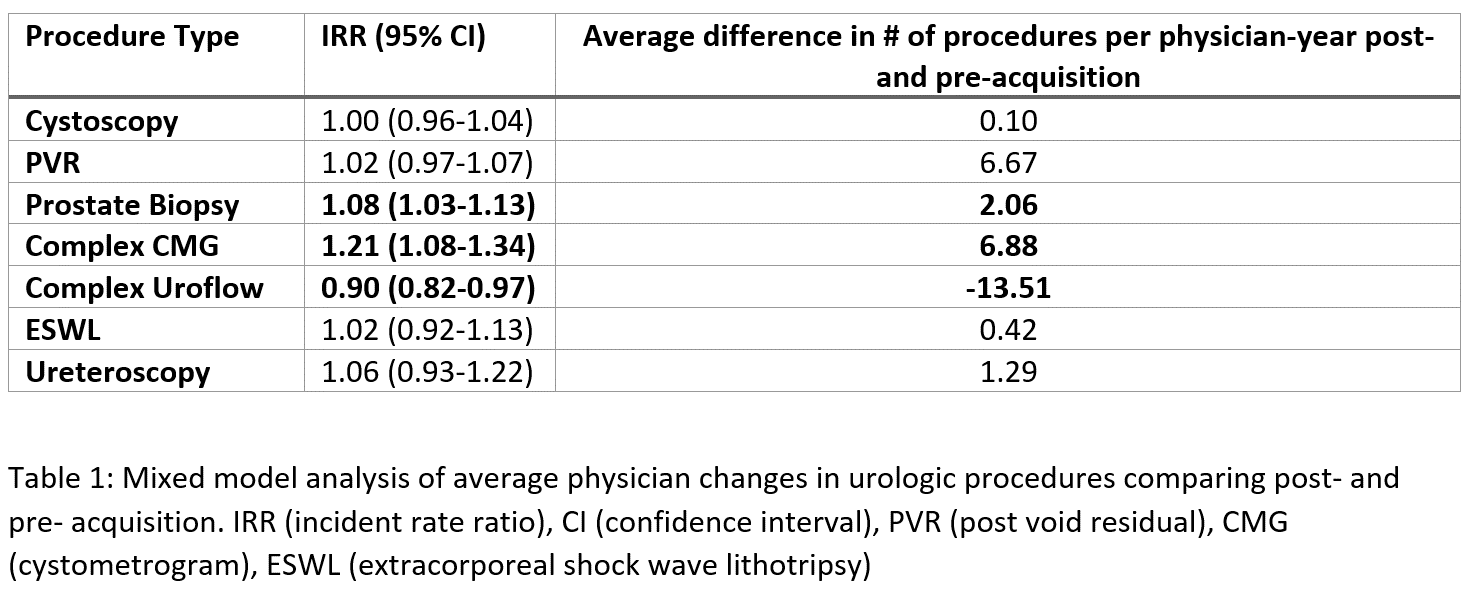

Introduction: Private equity firms have been increasing investment in urology in recent years. Despite the changing ownership model in urology private practice, the effect of these acquisitions on urologic practice and procedural volume has yet to be determined. We sought to investigate the impact on procedural volume in a variety of urologic procedures before and after private equity acquisition. Methods: Private equity acquisitions of urology practices were identified via the existing literature, which utilized a compilation of financial databases cataloguing both public and private transactions. Yearly office visit and procedure volume by provider was extracted from the publicly available “Medicare Physician & Other Practitioners by Provider and Service” dataset from 2013-2019. The most commonly billed procedures were chosen for analysis: post-void residual (PVR), cystometrogram (CMG), uroflow, cystoscopy, prostate biopsy, extracorporeal shock-wave lithotripsy (ESWL), and ureteroscopy. Mixed regression model and sensitivity analyses were conducted. Results: 1,564,853 office visits and 867,216 procedures were analyzed over a 5-year period. Using mixed model analysis, the number of cystoscopies, PVRs, ESWL, and ureteroscopies per physician-year showed no statistically significant change after private equity acquisition (Table 1). Prostate biopsy and complex CMG showed statistically significant increases by an average of 2.06 and 6.88 procedures per physician-year respectively after private equity. Complex uroflow had a significant decrease by an average of 13.5 procedures per physician-year after acquisition. The average number of each urologic procedure per 100 visits remained stable from before private equity acquisition to after acquisition. In terms of the average number of new patient visits, the observed trends for 30-, 45-, and 60- minute visits per 100 visits remained stable from before to after private equity acquisition. Conclusions: In this study we demonstrate the impact of private equity ownership on urologic practices before and after acquisition. We found that both prostate biopsy and complex CMG procedures rates increased significantly since private equity acquisition. The fiscal impact of these changes has yet to be determined. SOURCE OF Funding: N/A