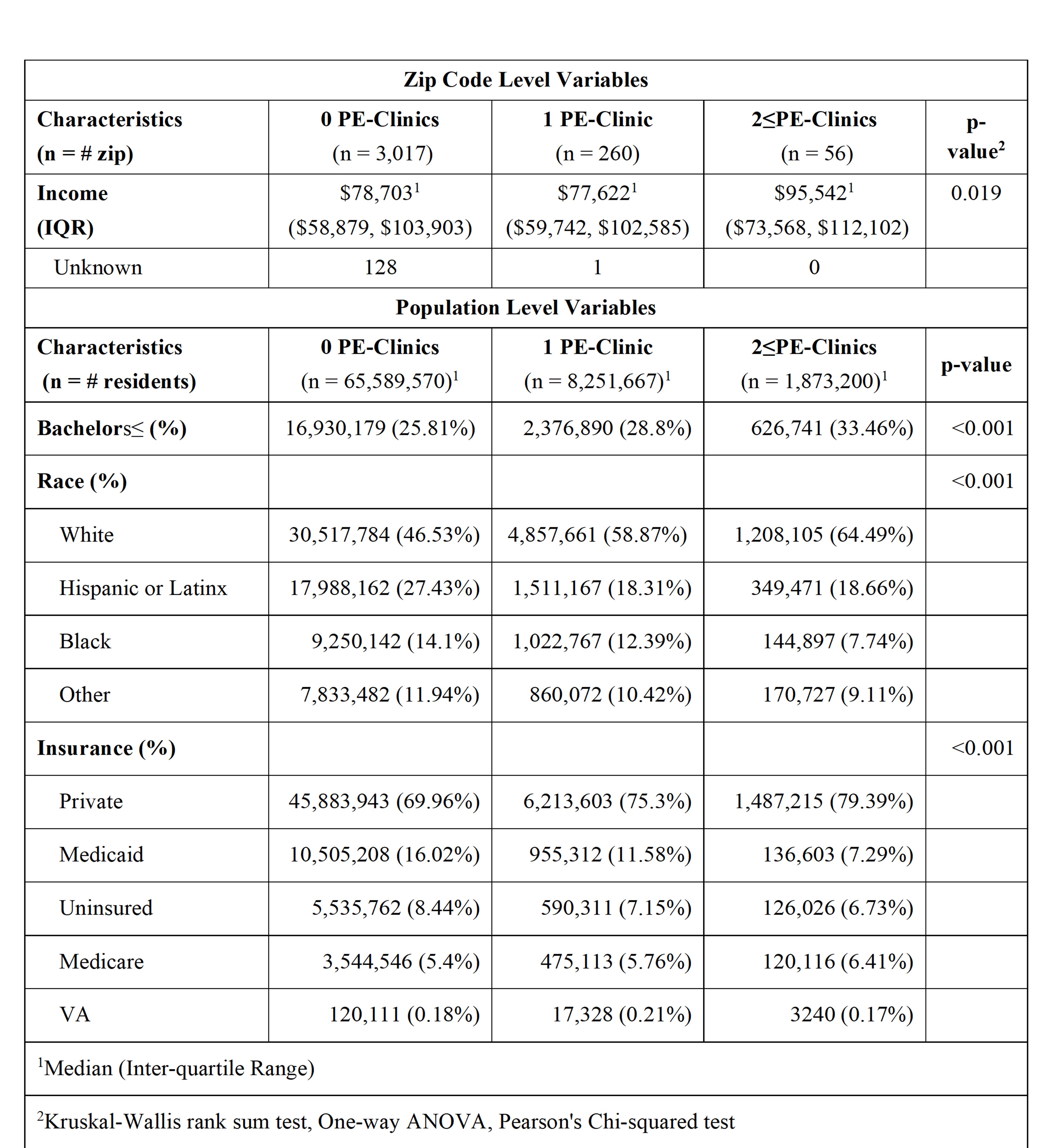

Introduction: Private equity involvement in healthcare has increased rapidly over the past 20 years, but the first urology practice was not acquired until 2016. After acquisition of a medical practice, private equity firms commonly deploy a “buy and build” model where they increase revenue and decrease costs to grow practice valuation before selling the practice within 5-7 years to a larger private equity firm. This study aimed to describe the private equity-ownership in urology practices and identify key characteristics of the populations these clinics serve. Methods: We identified private equity-owned urology practices from February 25, 2022 through May 31, 2022. Practice acquisition was confirmed by cross referencing news releases, platform websites, and Pitchbook (a comprehensive market data warehouse). Population-level data was obtained from the U.S. Census website for each zip code tabulation area (ZCTA) within each county that had at least 1 private equity-owned urology clinic. Zip codes were converted to ZCTAs for analysis using a crosswalk. Zip codes containing private equity-backed urology clinics were compared to zip codes that did not contain a private equity-backed urology clinic but were in the same county. Data was analyzed using one-way ANOVA, and Chi-squared tests of significance. Results: As of June 2022, 7 private equity platforms operate 387 urology clinics in 18 states, across 100 unique counties and employ 731 urologists. Zip codes that contained private equity-backed urology clinics (n=316) had higher rates of residents with a bachelor’s degree or higher, higher median family incomes, more white and less African American and Hispanic residents, and a greater proportion of privately insured residents than zip codes that did not contain a private equity-owned urology clinic (n=3,145, Table 1). These differences were universally amplified in zip codes that had higher concentration of PE-owned clinics (2 = private equity-owned urology clinics). Conclusions: Private equity ownership in urology has grown significantly since the first acquisition and is concentrated in areas of higher socio-economic status and less racial diversity. If there are quality benchmarks that are improved by private equity acquisition, those benefits are being disproportionally directed at wealthy and largely white communities thus far. SOURCE OF Funding: NIH/NIDDK University of Pittsburgh O'Brien Cooperative Research Center Program (U54 DK112079)

photo")